Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Should You Refinance Your Mortgage?

By Erin Wright & Christina Waterhouse

Questions to Ask and Information to Gather Before You Refinance

Low interest rates are attracting more and more people to the market, especially those who are looking to refinance their mortgages. Clients have been reaching out to us to ask if they should be refinancing their homes. Our general response is, “it depends”. There are a few questions and pieces of key information you should gather before deciding whether to refinance.

With interest rates at an all time low, everyone should ask, “Is refinancing a good decision for me?”

1. What is the difference between your interest rate and current interest rate?

A good rule of thumb is for the current rate to be at least .5 – .75% less than your interest rate. This rule can change greatly depending on the size of the loan though. The more money that is being borrowed, the larger the difference is going to be in both your monthly payments and your total interest paid. You can find the daily interest rate here.

2. How close are you to paying off your mortgage

At the beginning of a loan, most of the monthly payment is going to interest. Only a small portion of the payment goes towards paying off the principal balance of the loan. As payments continue, the amount that goes towards interest goes down and the amount that goes towards the principal balance goes up. It is worth looking at an amortization schedule to see if refinancing will save you money over the life of the loan. You can find an amortization calculator here.

3. Has your credit or employment changed?

Employment history, debt to income ratios, and credit scores all impact the rate you will receive when applying for a loan. Speak to your lender regarding any changes in these areas to make sure you would qualify for a refinance and see what rate you would likely qualify for. Then you can determine if it is worth refinancing.

4. What is the property being used for?

Properties that are used as primary residences qualify for lower interest rates than those used as investment properties (usually .5 – 1% lower). If you purchased the property as a primary residence and subsequently turned it into a rental, you might not see much of a change in your interest rate or possibly your interest rate as an investment property could be higher. Speak with your lender to see what the current interest rate would be for the specific property.

5. Should you refinance into a 15 year loan or 30 year loan?

If you do decide that it is worth refinancing your loan, consider looking at both a 15 year and 30 year loan. Right now the interest rate for a 15 year loan is in the mid 2% range, while the interest rate for a 30 year loan is in the high 2% range. A 15 year loan will save you a lot of money in interest over the life of the loan. This is a great way to build strong equity in your property and pay it off in half of the time.

As always, we welcome any questions you may have and are happy to offer advice.

Mortgage insight and references provided by: Mathew Mattila, Cascade Northern Mortgage

Real Estate and Covid–19 Part 2

Understanding Why Interest Rates Impact Buyer Activity in the Market

By Erin Wright and Christina Waterhouse

Last week we reviewed the overall Real Estate Market in Clark County since the start of the pandemic. This week we are looking deeper into why interest rates are impacting buyer activity.

Interest Rates, Buying Power, & Inventory

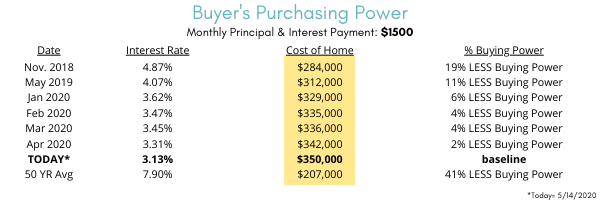

Home buyers have seen historically low interest rates since the end of the Great Recession, between 3% and 5% roughly, compared to the average mortgage interest rate over the last 50 years of 7.91%.[1]

Since the start of the current pandemic, interest rates have continued to lower. The rate as of today (Thursday, May 14, 2020) is 3.13%.[2] In the chart below, you see that even the small changes in interest rates from about 18 months ago until today make a big impact on buying power. This is crucial because in a market like Clark County where there is a housing crisis due to the rapidly rising cost of real estate, more buying power opens up more inventory. Just since the start of 2020, Buyers looking for a $1,500 payment a month for principal and interest (not including taxes and insurance) saw their borrowing power increase from $329,000 to $350,000. To showcase how this impacts their choices, we ran a search on Redfin for a detached, single family home in Clark County. There are currently 28 houses listed for sale up to the price of $325,000. When we move that budget up to $350,000, there are 80 houses listed for sale. Just that $25,000 increase in budget, returned 3x the inventory on the market.

Interest Rates and Monthly Payments

Let’s also look at how the interest rate impacts a monthly payment and therefore a buyer’s monthly budget. In the chart below, you can see how the interest rate would impact a monthly payment for principal and interest (not including taxes and insurance) if a buyer purchased a house at an interest rate from 18 months ago, the beginning of this year, and today. There is a 23% difference in the monthly payment from the most recent high interest rate in November 2018 vs the interest rates today. For a $400,000 house, that equates to an extra $400 a month. This is important because even though some buyers are qualified to purchase a house, they do not feel comfortable spending more than a certain amount per month on their housing. With the interest rate saving $100’s of dollars a month, new buyers will be able to feel comfortable entering the market.

With Buyers able to enter the marketplace and have more buying power since the start of the pandemic, there is still a demand to purchase real estate. As we discussed last week, this demand mixed with fewer new listings coming on the market that would typically be seen this time of year has led to a strong Sellers’ market. The current demand mixed with the lower supply has kept prices stable even during a pandemic with high unemployment.

Mortgage insight and references provided by: Mathew Mattila, Cascade Northern Mortgage: https://www.mathewmattila.com/

As always, we welcome any questions you may have and are happy to offer advice.

[1] History of Monthly Interest Rates According to Freddie Mac: http://www.freddiemac.com/pmms/pmms30.html

[2] Daily Interest Rates According to Mortgage News Daily: http://www.mortgagenewsdaily.com/data/30-year-mortgage-rates.aspx